Inflation continues to be a worry for many investors. A variety of inflationary measures continue to run hot and above the Fed’s 2% target. Meanwhile, tariff worries and supply chain changes have the potential to keep the invisible hand of rising prices growing in the quarters ahead. For many investors, fighting inflation has become a full-time job.

But it doesn’t have to be. There is one boring asset class that actually holds its own when it come to inflationary environments.

It turns out that staid municipal bonds have managed to outperform in periods of high and steady inflation. Thanks to several key attributes, munis offer a strong return and income element during periods of sustained and high inflation. Given the uncertainty surrounding inflation and the overall market, boring munis could be worth a look.

Inflationary Worries Persist

Stubborn would be the best adjective to describe inflation these days. As pandemic-era stimulus met headfirst with a snapback in demand, inflation spiked in 2022 and 2023. After peaking at 9.1% in June 2022, the invisible hand of rising prices has spent much of the last two years shrinking. By all accounts, the Fed has done a great job of reducing the post-pandemic high.

The latest CPI report — released for April’s figures — shows an interesting and complex picture for rising prices. For the month, CPI rose by a seasonally adjusted rate of 0.2%. This has put the 12-month inflation rate at 2.3% — the lowest reading since February 2021, according to data from the Bureau of Labor Statistics. That’s the good news.

The problem is, inflation hasn’t fully gone away.

2.3% is still above the Fed’s target of 2%. Moreover, the outlook doesn’t look so good. Inflation is expected to rise further as consumers and businesses grapple with a differentiated supply chain and costs due to the pending Trump Administration tariffs. Expectations for inflation are now higher … by a lot. According to the University of Michigan consumer survey, year-ahead inflation expectations are now at 7.3%, while long-term inflation expectations ticked up to 4.6%.

While there are many moving parts to all of this, the underlying point is that inflation isn’t going away completely, and we still could experience some elevated price increases or stubborn inflationary pressures for the long haul.

Munis to the Rescue

The municipal bond sector is arguably one of the most boring segments of fixed income. There’s a good reason for that. Bonds issued by states and local governments are used to fund day-to-day activities, special projects, and other needs. Because they are backed by tax or project revenues, investors do not consider them risky.

So, it’s strange to think of these boring bonds as great inflation fighters. But it turns out, they are.

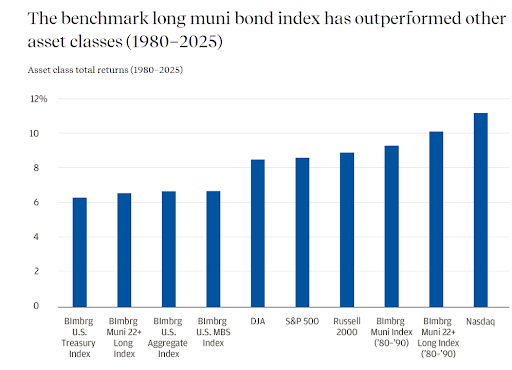

According to a white paper from J.P. Morgan, muni bonds have outperformed Treasuries over the long haul, as well as during the last period of high inflation. The Bloomberg Municipal Long Bond 22+ Index has returned 6.57% on average per year since 1980. That managed to beat the Bloomberg U.S. Treasury Index over the same period.

What’s interesting is that during the periods of high inflation, in the 1980s and the 1990s, both the Muni Long Index and the short-dated Bloomberg Municipal Bond Index outperformed the major stock indices — the S&P 500, Dow Jones Industrial Average, and the Russell 2000 during that— time. This chart from the investment bank highlights the strong returns.

Source: J.P. Morgan Asset Management

Ultimately, municipal bonds have historically proven to be better inflation hedges than the broader stock market. The reason why comes down to uncertainty, high after-tax yields and how munis generate their coupons.

For starters, the way municipal bonds generate their coupons is a key reason why they’ve managed to perform well against inflation. As we mentioned, munis are issued to help finance state or local government expenditures. With that, the State of Texas or the City of Anaheim can raise taxes to cover their bonds if there’s an issue. However, that’s just one side — so-called general obligation (GO) bonds — of muni bonds.

The other are munis issued to pay for specific projects. These are revenue-backed bonds. Often, prices to use these projects — tolls, public utilities, education, mass transit — move higher along with the CPI. This provides inflation-protected revenue streams. Because of this, investors often will go to munis when inflation spikes. The coupon payments are protected on multiple fronts.

Muni’s also win on their after-tax benefits. Because many municipal bonds are free from Federal taxes and potentially free from state taxes as well, this provides an additional advantage during periods of high inflation. For taxable bonds, investors lose a greater portion of their interest due to taxes and higher prices. But with munis, they only have to contend with higher prices thanks to inflation, not both. This provides them with extra appeal as inflation rises. Their coupons become that much more valuable versus a regular taxable bond.

Munis Make Sense Today

Given the rising inflation potential of the tariffs and various tax policy choices, municipal bonds present an interesting option in the current environment. With yields still high and inflation remaining steady, potentially rising, the bond type can offer some downside protection as well as a way to beat inflation. After-tax yields, along with the stability of the coupon payment, underscore the bond’s appeal today.

With that in mind, investors may want to consider municipal bonds (munis) for their bond portfolios.

As we’ve said before, getting your hands on individual muni bonds can prove to be difficult. That means using funds is the best option, both passive and active, to build an allocation.

ETFs —both active and passive — can be used to achieve a strong mix of traditional and non-traditional bond sectors, fully embracing the opportunities in bonds.

Municipal Bond ETFs

These ETFs were selected based on their exposure to municipal bonds at a low cost. They are sorted by their YTD total return, which ranges from -1.7% to 1%. They have expense ratios between 0.03% and 0.65% and assets under management between $1.5B and $41B. They are yielding between 2.3% and 3.4%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| SUB | iShares Short-Term National Muni Bond ETF | $9B | 1% | 2.3% | 0.07% | ETF | No |

| SHM | SPDR Nuveen Bloomberg Short Term Municipal Bond ETF | $3.5B | 1% | 2.6% | 0.20% | ETF | No |

| DFNM | Dimensional National Municipal Bond ETF | $1.5B | -0.1% | 3.1% | 0.18% | ETF | Yes |

| MUNI | PIMCO Intermediate Municipal Bond Active ETF | $1.8B | -0.2% | 3.3% | 0.35% | ETF | Yes |

| FMB | First Trust Managed Municipal ETF | $2.1B | -1.6% | 3.4% | 0.65% | ETF | Yes |

| MUB | iShares National Muni Bond ETF | $41B | -1.6% | 3.3% | 0.05% | ETF | No |

| VTEB | Vanguard Tax-Exempt Bond ETF | $39.5B | -1.7% | 3.4% | 0.03% | ETF | No |

Ultimately, muni bonds offer a great blend of strong coupon repayment and after-tax benefits that help deliver strong gains during periods of high and rising inflation. With various market and fiscal forces now potentially reigniting inflation higher or, at best, keeping it the same, investors still need to fight inflation in their portfolios. Munis can help deliver in that fight.

Bottom Line

Inflation remains stubborn, and investors shouldn’t overlook munis in that battle. Thanks to several attributes, such as high after-tax yields, munis make a ton of sense for a portfolio today.